by W. Robert Pearson

Türkiye’s 2001 Financial Crisis

On February 19, 2001, at a formal government meeting, the president of Türkiye, Ahmet Necdet Sezer, accused the prime minister, Bulent Ecevit, of incompetent management of the country’s banking system and threw a copy of the Turkish constitutional code book across the table at him. The prime minister stormed out, called a press conference, and verbally attacked the president. Immediately, the stock market panicked, the lira plunged, and interest rates skyrocketed.

My wife Maggie and I were celebrating a belated Valentine’s lunch that day. An embassy colleague rushed in to say the Turkish lira was crumbling. I called the prime minister and urged him to buy lira with Turkish reserves as fast as possible. He ignored my advice and by day’s end the lira was in the basement. Overnight, the savings of many ordinary citizens were devastated, and millions of dollars of value had vaporized.

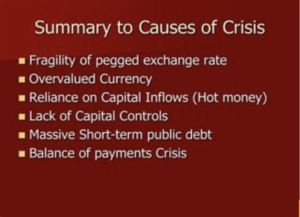

The causes of the collapse were many. Türkiye had experienced high inflation throughout the previous decade. The government had run large deficits and funded them with high interest bonds that avoided short-term defaults. The increased borrowing and growing public debt created a dangerous economic risk. The Turkish banking sector faced significant issues, including inadequate regulations, poor risk management, and high levels of non-performing loans. Many banks had debts that were difficult to collect. Türkiye depended greatly on foreign borrowing to finance its economic growth, but, as economic imbalances worsened, changes in investor sentiment added to concerns. Foreign investors withdrew over $70 billion from 2000 to 2001 as the economic situation deteriorated.

Strong rumors indicated that the government periodically ordered new funds from the central bank and channeled the monies to its coalition political parties, and these rumors of corruption eroded public confidence. Türkiye had pegged its currency to a calendar schedule to control speculation, but the effect actually was to overvalue its currency against the dollar. Black market speculation began to balloon. The current account gap grew as exports were less competitive. The damaging results of the Asian financial crisis in the late 1990’s and the Russian financial crisis in 1998 on Türkiye’s economy had already added to the ongoing erosion of public confidence. The February 19 political outburst shredded Türkiye’s economic house of cards.

Before the crisis the US Treasury had used several trips to Türkiye by its undersecretary to admonish the Turks to move off the peg to a more flexible exchange lira. The government always expressed confidence that the pegged schedule would work. In reality, the government feared that letting the lira float would precipitate a crisis, not avoid one. The government’s reasons were correct for its temporary survival, but the alternative was to watch and wait for the inevitable economic earthquake.

Before the crisis the US Treasury had used several trips to Türkiye by its undersecretary to admonish the Turks to move off the peg to a more flexible exchange lira. The government always expressed confidence that the pegged schedule would work. In reality, the government feared that letting the lira float would precipitate a crisis, not avoid one. The government’s reasons were correct for its temporary survival, but the alternative was to watch and wait for the inevitable economic earthquake.

Putting Together a Recovery Plan

Following the meltdown, the American Treasury was not immediately in favor of a major program to help Türkiye recover. When I asked the Treasury to join with the IMF to put the elements of a program together, Treasury declined, wishing to have more control over any recovery. I knew that US help was indispensable, however, and knew that the sooner that help appeared the more lasting and deep would be the recovery. I knew as well that an acceptable plan required that it be seen as a Turkish initiative, not a program imposed by American economic guidance.

Kemal Dervis, a former World Bank vice president, superb economist, deeply experienced, and later the administrator of the UN Development Program, was the key to opening the door to recovery. I had a problem; when I had requested through US government channels a meeting with the IMF, the Treasury blocked the meeting request. I turned to Kemal Dervis, at that point a close friend, to ask for help. He knew Anne Krueger, a highly respected American economist who was the managing director of the IMF at that time and instrumental in shaping IMF policies and operations. Rather than further tussle with the Treasury, I asked Dervis to ask Dr. Krueger if she would invite me to lunch on an upcoming trip to Washington.

I shortly received an invitation for lunch. When the Treasury asked about the meeting, I invited them to send a note taker but not to engage in the conversation since it was a personal invitation. I laid out the case for Türkiye to receive substantial assistance and put heavy emphasis on the reform program that Kemal Dervis had underway. Dr. Krueger was familiar with Türkiye and its economy and clearly understood the effect financial loan assistance would provide to Türkiye. She also knew Dervis well. I thanked her for the opportunity to put forward the case regarding Türkiye.

Shortly thereafter, the IMF began its work. In the end, the IMF approved a Stand-By Arrangement for Türkiye in December, 2001 with a total value of $16 billion provided in installments over the course of the program. Release of those installments required Turkish structural reforms ranging from banking sector reforms, fiscal consolidation measures, and improvements in economic governance to restoration of macroeconomic stability by targeting inflation reduction, fiscal discipline, and exchange rate flexibility. The IMF oversaw the implementation of the reform program, conducting regular reviews to assess progress and provide guidance, and technical assistance and expertise in areas such as fiscal policy, monetary policy, banking sector supervision, and debt management.

Economic Recovery 2002-2010

The crisis brought about a deep political change in Türkiye in 2002. The disappearance of the 2001 government coalition in the 2002 general election marked the end of the Kemalist heritage of governance in Türkiye after a reign of 75 years. The new Islamist government – the Justice and Development Party (AKP) – represented a sharp departure from the secular political legacy of Türkiye. The AKP government understood the popularity of the reform program and continued it, while claiming the program as its own creation.

The work undertaken in 2001 and 2002 continued to foster sustained economic growth in the first decade of the 2000s. During the period 2002 to 2010, Türkiye’s GDP increased by about 2.6 times with an average annual growth rate of 6 percent. The recovery buffered Türkiye during the start of the worldwide recession in 2008-2009 and moved the country to a higher ranking among world economies.

Regression 2010-2020

During the 2010-2020 period, the Turkish economy saw positive growth rates, substantial investments in infrastructure, and increased tourism. Foreign direct investment (FDI) continued, but Türkiye’s global share of FDI fell back to early 1990s levels. Policies that led to Türkiye’s 2001 economic meltdown began to reappear. The current account deficit grew, inflation became rampant due to bizarre governmental economic policies, unemployment grew, and the lira’s value repeatedly tumbled. Transparency, accountability, and the rule of law came into question. Türkiye’s increased private sector debt, often in dollar denominated instruments, affected financial stability, and banking sector non-performing loans drew attention. Türkiye’s rank in world economies has slipped from 16th place 20 years ago to 19th today. Türkiye’s oft stated ambition over the years to become a top 10 economy doesn’t seem to be any closer now. Once again, Türkiye may be racing against the economic clock.

Is There a Future for US-Turkish Economic Cooperation?

Türkiye’s president, Recep Tayyip Erdogan, elected for a third term in May 2023, has brought his widely respected former finance minister, Mehmet Simsek, back to his old job. Simsek promises a gradual shift to conventional economic policy. The new central bank governor is Hafize Gaye Erkan, former co-CEO at the First Republic Bank and managing director at Goldman Sachs. She becomes Türkiye’s fifth central bank governor in four years and faces the challenge of re-establishing the bank’s independence and achieving a lasting policy redirection. Currently, projections have government interest rates running well below inflation rates with gradual improvement over the next two years. Eyes will be riveted on President Erdogan in coming months as these two experts with sound economic reputations try to rebalance the economy. That rebalance is essential to Türkiye’s attracting more foreign direct investment, without which the economy risks sinking further in world ranking.

Recently, a venture capitalist who concentrates on Türkiye’s small and medium sized economy for investment opportunities told me that Ankara expects inflation to peak in 2024. If so, the government, he says, will raise post-peak inflation wages to compensate. The combination of a rise in wages and a lowering inflation rate would soften the subsequent impact of inflation even if government interest rates are lower than the inflation rate for a further time.

There is a need for Türkiye to become a strong and stable economy. At the moment, it is likely that the country will find itself under economic pressure throughout 2024. To date, Turkish and US economic cooperation has been adversely affected by President Erdogan’s haggling over support for Sweden’s NATO membership and by his attacks on Israel and support for Hamas. That picture could be changing. The New York Times reported that the State Department notified Congress on January 26 that it had approved the $23 billion sale of F-16s to Türkiye upon receipt of the proper documents from Ankara approving Swedish membership of NATO. According to the report, senior Congressional leaders indicated after examining the Turkish documents that they will not oppose the sale. Approval of the deal will open a new opportunity for broader US-Turkish cooperation to realize the enormous potential of a healthy Turkish economy. Mr. Erdogan is not good at statesmanship. Let’s see if he can rise to the occasion this time.![]()

Ambassador W. Robert Pearson is a retired professional Foreign Service Officer who was director general of the US Foreign Service from 2003 to 2006, repositioning the American Foreign Service to meet the new challenges of the 21st century and winning two national awards for his efforts. He was US ambassador to Turkey from 2000 to 2003. Ambassador Pearson served as executive secretary of the State Department and on the National Security Council in addition to assignments in China and NATO and other overseas posts.